A while back, I sent out a Money Tip to my mailing list about the dangers of loss aversion and sunk costs, two pervasive financial challenges described in behavioral economics. A reader, Mia, reached out with a funny, related story about her cappuccino maker. I’ll get to that in a second. First, though, here’s the core of what I said to my readers.

Look in the mirror. You’ll see the reflection of your greatest friend and a persistent pain in the backside when it comes to your finances. Actually, you can’t see your frenemy because it’s inside your skull. I’m referring, of course, to your brain.

Let’s take a quick look at two of the ways in which our brain wreaks havoc on our finances.

Loss Aversion

According to research, it seems we all care deeply about losses. To be sure, we’re also interested in gains, but not nearly as much as losses.

Why? Because we value gains and losses differently.

The work of two famous (and Nobel-winning) behavioral economists, Daniel Kahneman and Amos Tversky, demonstrates that we hate the idea of a $10 loss more than we love the idea of a $10 gain.

The pain we feel in the one instance is much greater than the pleasure in the second instance, even though the amounts are exactly the same – $10 either way. According to Kahneman and Tversky, “we feel the pain of losing $10 about twice as strongly as we do the pleasure of winning $10.”

This is a problem for our finances. Marketers are well aware of this human bias and they milk it for all it’s worth when they pitch offers like the following:

- Don’t miss out on the big savings!

- Buy today to ensure you don’t lose out on this opportunity!

- Only one seat left! Purchase your ticket before they’re all gone.

- If you sign the contract today, we’ll throw in floor mats.

Heaven forbid you should miss out on the floor mats, the one remaining seat, and all the purported savings from the sale. If you don’t act now (i.e. spend money), you’re losing out. The unspoken message is that you’ll end up spending more money, therefore, you’re a loser. Literally. It’s hogwash, but that’s precisely what marketers want you to think.

So, you spend money on things you don’t need, don’t really want, and don’t value. Floor mats, people; floor mats!

You placate your wise financial self with the illusion of having made a smart financial decision. “Look at the bright side – you didn’t lose out!” you think to yourself.

Really, though, you have lost out, because you’ve spent money you did not really want or need to spend.

Loss aversion affects every aspect of our finances. It makes us procrastinate about saving and investing for retirement. Future gains (i.e. comfortable retirement) are far less compelling than the pain of taking money our of our cash flow today. That hurts!

Investing in the stock market is an area where loss aversion is hard at work. We could lose money, which is scary; so, we avoid it or we bail on our investments at the first downturn in the market. Never mind that over the long run, the market generates consistent growth. It’s the dips in the short term that that trigger avoidance behaviours.

Even when our employers offer to match our registered retirement contributions, up to a certain amount, we STILL don’t participate fully, if at all. We actually give up free money! Think about that – turning down free money.

Sunk Costs

To add insult to injury, once we have purchased something we don’t need and may not really want, we hold on for dear life because, damn it all, we are going to get our money’s worth. Here’s the thing: the money is already spent and we can’t get it back. That’s the sunk cost part.

Have you ever bought tickets to an event, then a snow storm hit or you developed a nasty cold and you really shouldn’t have gone, but you dragged yourself out to the thing anyway? Even though you were miserable the whole time, or you took serious risks getting there on icy roads?

That’s the fallacy of sunk costs at play as well. Instead of buying tickets and viewing them as an option, whether we exercise it or not, we get stuck on the fact that we’ve spent good money and we are going to make use of the thing/tickets/whatever regardless of the fact that the best course of action would definitely be to stay home. We do that because it feels like we’re losing money if we don’t use the tickets, when in fact the money has already been spent. It’s long gone, regardless of the outcome.

Snowmageddon

I learned this the hard way when we first started using a snow removal service. One year, when my girls were just babies, my husband left for a week-long business trip. In his absence, 51 centimeters of snow fell in one day. (That’s nearly two feet for those who speak American.) At that time, we didn’t have a garage, which meant that our car was buried in snow. In order for me to get out of our driveway, I had to shovel it myself. I should also mention that there had been an insane amount of snow in the weeks prior to that, which meant that there were massive snow banks adjacent to our driveway.

Out I went, with the baby strapped into a car seat just inside the front door where I could see her and my 3 year old “reading” to her while I heaved snow up onto the “mountains”, as my oldest called them. I shoveled on and off over the entire day. “Never again,” I said.

When we moved to a larger house, we paid for a snow removal service. That first year, it worked brilliantly. A ton of snow fell and all of it, except the front steps, was removed by a tractor. Satisfaction. I felt so smart. Then the next year, we barely had any snow. It felt like we had paid $450 for nothing. What a waste. Surely there’s a better use for our money? I decided not to renew the following year since I had not received my money’s worth the previous year.

At this point, you know exactly what happened: Mother Nature opened up the skies and taught me a lesson I will never forget. My husband had tried to warn me at the start of the season. “Doris,” he said, “the service is an insurance policy. It’s a sunk cost. We’re paying for the possibility of using it. If we do, great. If it doesn’t snow much, we shrug. That’s how it goes. But we should definitely pay for it and not stress about what happens with the weather. We can’t control that.” So sensible and so right. Me? So stubborn and sucked in by the siren call of Loss Aversion and Sunk Costs.

One month into the winter season, I called our snow removal company and booked the service. I was happy to pay and I have not since cared about the number of snow flakes landing on my driveway.

Helpful hacks

Loss Aversion and Sunk Costs aren’t something you can get over. They’re deeply ingrained human biases to which we all fall prey. That said, we are not helpless creatures. Here are a couple of ideas to help you counteract their effects:

1. Pause before you hit the “Buy Now” button. Ask yourself if the purchase is truly something that fits into your values-based goals and your ensuing financial plan. Sales come and go. Forget about sales pitches. Stick to your plan, your shopping list, and your goals. Ignore the hype.

2. Make conscious choices after considering both sides of the equation. If you’re told that you have a 20% chance of losing, you also have an 80% chance of winning. If you’re not sure about a decision, run the options by a trusted source who can test your assumptions.

3. Ignore the cost when deciding what to do about an item. Once you’ve purchased something – a cappuccino maker, for example (coming up next), tickets, or whatever – accept that the money has already been spent. Do not think about the cost when deciding what to do in the future. The decision should be an independent one based on the best choice for you at that moment. Keeping an item you don’t use won’t make it more valuable to you. Taking risks or prolonging an illness to make use of tickets isn’t worth it. Cut the loss and move on.

4. Beware of sale signs and ignore the percentage off. A dress that you paid $250 for after a 50% reduction is still a $250 dress. Does that represent good value for that particular item? Do you need it? Is it something you value? These are much more helpful questions to ask. Remember that the sale sign may benefit the seller more than you.

Mia and her cappuccino maker

When I asked my readers to send me their stories of loss aversion and/or sunk costs, I received the following from Mia*:

I’m typing this email at my kitchen island, from which I can stare across at my expensive and fancy cappuccino maker that I’ve messily/unsuccessfully made one cappuccino with in ~3.5 years. I even moved the box. BECAUSE IT COST OVER 200$. I wasn’t even making coffee daily at the time, I just liked the idea of being the type of person who owned a cappuccino machine.That’s something I’m trying to be conscious of while I’m prepping for my move, as I edit my belongings. What am I holding onto because I like the idea of being the type of person who has that thing/reads that book/wears those clothes? Some of my purchases (not many within the last two years, but certainly in the last decade, as my disposable income increased) were aspirational in nature. I’ve learned lots about who I really am and what I really like based on the books I didn’t end up reading or clothes I haven’t worn in 5 years (*cough* 180$ Little Black Dress I wore to one event which might not even fit anymore, since I’ve been [exercising] very seriously *cough*).

You won’t believe it, but Mia’s damn cappuccino maker is in a box bound for B.C. right now….

Coffee maker in the box:

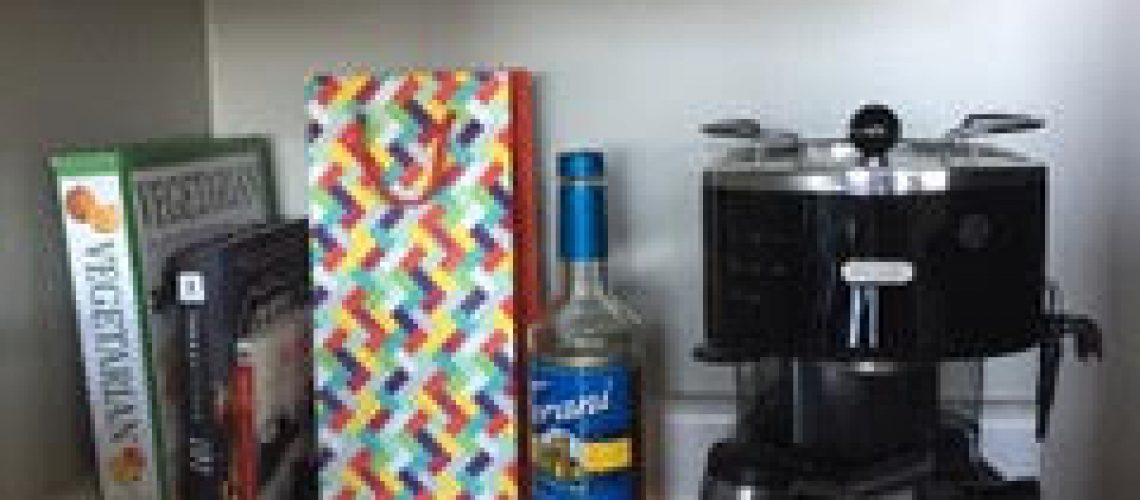

Coffee maker out of the box, next to the wine (in colourful bag):

Mia thinks the coffee maker looks GREAT on her new counter. She took it with her because she didn’t take the time to sell it before her move. Now, it’s almost like a joke, to carry this symbol of sunken cost around with her, to remind her to think twice about making big new shiny purchases.

I think it’s hilarious that she now refers to herself as Mia, since that’s not her real name. (I always do two things when I share people’s stories: I get their permission and I change their names.) At first, I found it amusing that the thing ended up back on her counter top after a cross-country move. Then I thought, you know what? That’s not a bad idea. Keeping a symbol, front and center, of a lesson learned is useful. My husband keeps a copy of a Nortel dividend cheque for pennies – literally nine cents – in his office as a reminder of a harmful decision driven by loss aversion. I have a share certificate for a company nobody’s ever heard of that doesn’t exist anymore. Goodbye $$$.

Lesson learned.

What’s your story?

How has loss aversion affected you in the past?

What decisions did you make to avoid losing money?

What did you buy to ensure you didn’t miss out on a “great sale”?

Which item or investment did you hold on to far too long for all the wrong reasons? (Real estate money pit, anyone?)

Shoot me an email to let me know what you uncover. I’ll share more of my own and readers’ stories next week.